Discount #04 — What the Market Is Actually Pricing: Governance Risk

China's central SOEs generate higher ROE than private peers, yet the PB-ROE valuation framework completely fails on them. This installment examines why traditional fundamentals-based pricing breaks down on state firms — and what the 2023 reform does and does not change about governance risk pricing.

China's central state-owned enterprises pay higher dividends than private-sector peers. They generate higher returns on equity. Their revenue and profit growth held up better through the worst years of the past decade. Yet they trade at a structural discount that has not closed — even when individual companies, like COSCO Shipping Holdings at a 67% ROE and a 0.86x PB ratio in 2021, present what would be unmistakable arbitrage opportunities in any mature capital market.

The fundamentals do not explain the discount.

So what does the market believe it is pricing?

The honest answer — and the one this article will defend — is governance risk. The discount is not a mistake. It is a rational market response to a real structural feature of how Chinese SOEs are owned, controlled, and ultimately accountable.

This is the most uncomfortable article in this series. It is also the most important.

Where the Standard Model Breaks Down

The PB-ROE valuation framework is one of the most widely used tools in equity research. First articulated by Jarrod W. Wilcox in his 1984 paper, the framework rests on a simple proposition: a company's price-to-book ratio should reflect its return on equity. Companies generating higher ROE should command higher PB multiples, because higher returns on book equity translate into more value created per dollar of shareholder capital.

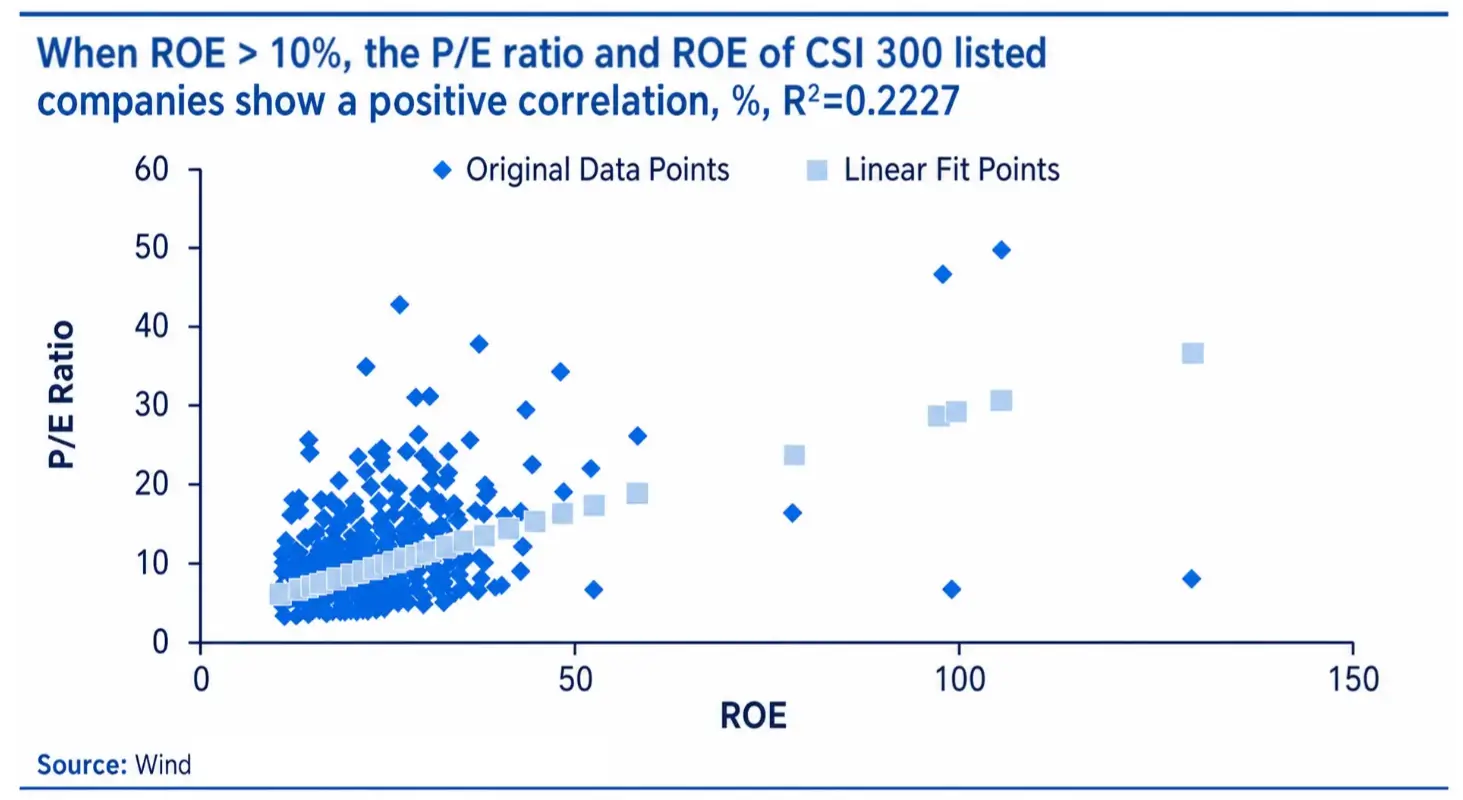

The logic is intuitive, and the empirical relationship usually holds. In a backtest of CSI 300 constituents — China's benchmark large-cap index — the PB-ROE relationship behaves as the model predicts when ROE exceeds 10%. The R-squared of the regression in this range is 0.2227: not perfect, but a meaningful positive correlation. Companies with higher returns on equity do, on average, trade at higher multiples to book value.

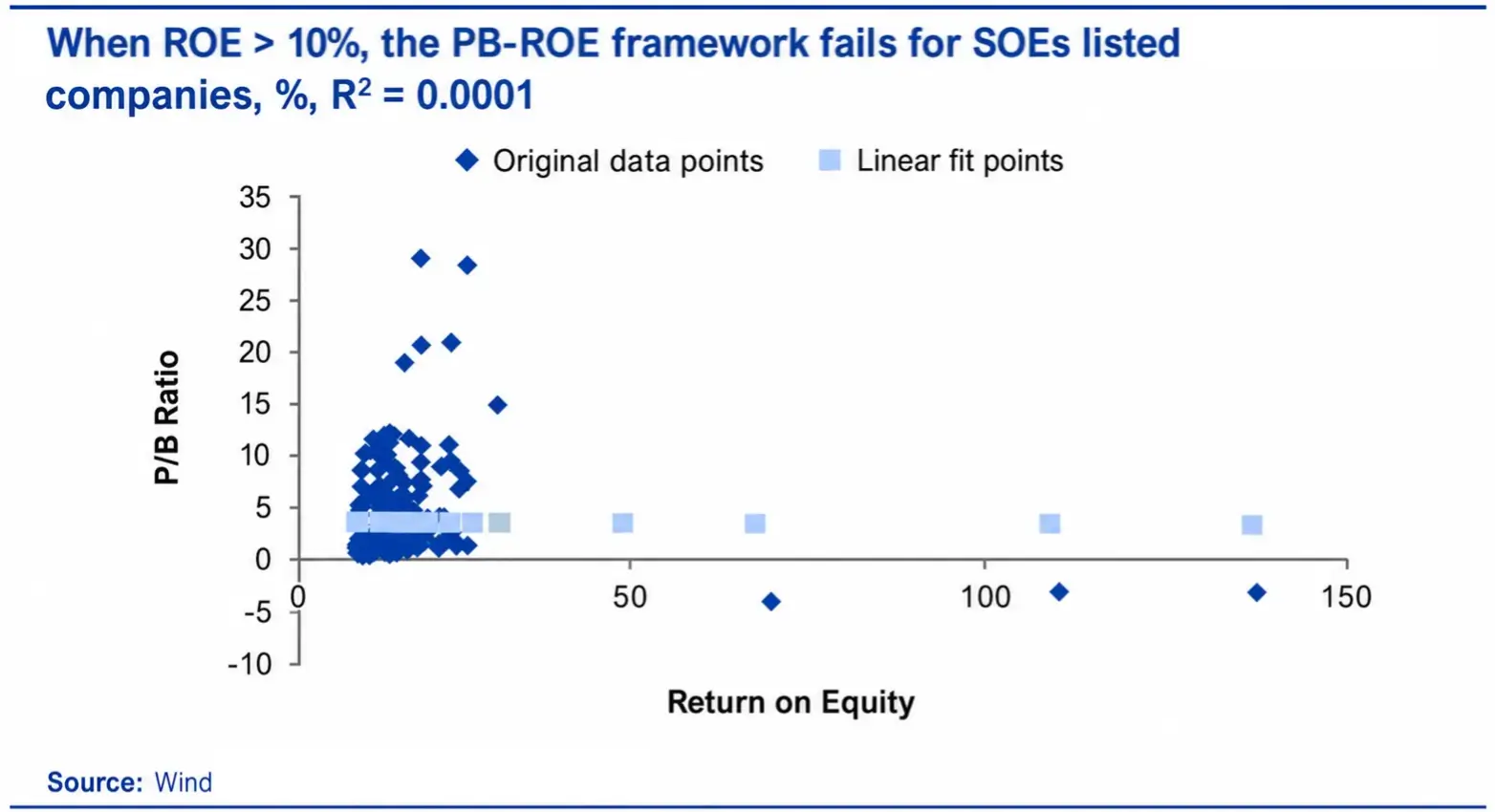

Now apply the same test to central SOE listed companies.

The R-squared collapses to 0.0001.

When you narrow the analysis to SOEs with ROE above 15%, the relationship turns negative — meaning that, within this subset, companies with higher returns on equity actually trade at lower price-to-book multiples than their lower-ROE peers. The framework that works for the broader market does not just fail on Chinese SOEs. It inverts.

This is not a small finding. It is the central diagnostic fact of this entire series.

What the Inversion Means

When a valuation model fails this comprehensively on a specific market segment, there are two possible explanations.

The first is that the model is wrong — that PB-ROE simply does not apply in the Chinese SOE context, perhaps because the underlying ROE figures are unreliable, or because some other measurement issue distorts the data. This explanation is convenient, but the data does not support it. The ROE figures for central SOEs are calculated using the same accounting standards as the rest of the A-share market. The dividend payout data, examined in the previous article, corroborates the cash-generation capacity that the ROE figures imply. The fundamentals are real.

The second explanation is that the model is correct, but it is being applied to data that the market is deliberately discounting for reasons the model does not capture. In other words, the market sees the same ROE figures the model uses, but applies a haircut to them — a discount that reflects something other than profitability.

That something is the credibility of the claim that minority shareholders will receive a proportional share of those returns.

Higher ROE only translates into higher equity value if shareholders can rely on capturing it. When that reliability is in question, the market does what any rational pricing mechanism would do: it discounts the future stream of returns to reflect the probability that some portion of those returns will be redirected to ends other than shareholder enrichment.

This is governance risk, and it is what the discount is pricing.

Three Sources of Governance Uncertainty

Naming governance risk is one thing. Specifying what makes it operative in the Chinese SOE context is another. There are three distinct mechanisms at work, and they reinforce each other.

The first is the historical priority of policy objectives over shareholder returns. Central SOEs are not, and have never been, organized exclusively around shareholder value maximization. They serve as instruments of industrial policy, employment stabilization, technology development, and regional economic balance. In normal times, these objectives align with profitability — a profitable SOE is a more useful policy instrument than an unprofitable one. But in periods when the objectives diverge, the historical record shows that policy considerations have taken precedence. Capital allocation decisions, pricing decisions in regulated sectors, and reinvestment patterns have all reflected mandates that minority shareholders had no formal mechanism to challenge.

The second is information asymmetry. Even by the standards of emerging-market disclosure, the gap between what central SOE management knows and what minority shareholders can independently verify is substantial. Related-party transactions with parent groups, capital reallocations within the SOE system, and strategic decisions made at the SASAC level rather than the listed-company level all create channels through which value can be transferred without conventional disclosure triggering. This is not necessarily a function of bad faith. It is a function of how the ownership structure is organized.

The third is the absence of standard governance disciplines. In a typical equity market, underperforming or value-destroying management faces several disciplining mechanisms: hostile takeovers, activist investors, proxy contests, and the implicit threat of a control transaction. None of these mechanisms function in the central SOE context. The controlling shareholder is the state, the state cannot be displaced, and the management that the state appoints cannot be removed by minority shareholder action. The traditional toolkit that minority shareholders elsewhere rely on to enforce governance discipline is simply absent.

The combination of these three factors does not mean that central SOEs are bad investments. It means that the standard valuation models, which implicitly assume a certain baseline of shareholder protection, do not translate cleanly. The discount is the market's adjustment for that translation problem.

Why 2023 Is Not a Cosmetic Reform

Now the second article in this series can be read in its proper context.

The "One Profit, Five Ratios" framework introduced by SASAC in January 2023 is often described as a performance management update — a refinement of how central SOE results are measured. Read against the governance risk problem this article has laid out, it is something more substantive.

For the first time, the framework formally ties senior management evaluation, compensation, and career outcomes to metrics that are aligned with shareholder interests: return on equity, cash flow quality, and profit growth relative to GDP. These are not soft targets. They are binding evaluation criteria.

This matters for governance risk pricing in a specific way. One of the three sources of uncertainty identified above — the historical priority of policy objectives — operates through the incentive structure of SOE management. When management is evaluated and rewarded primarily on policy execution rather than financial performance, the rational response is to prioritize policy. When the evaluation system shifts toward shareholder-oriented metrics, the rational response shifts with it.

The 2023 framework does not eliminate governance risk. It does not change the ownership structure. It does not provide minority shareholders with the disciplining tools they have in mature markets. What it does is change the incentive layer that sits on top of those structural features — and incentive change is the prerequisite for any sustained shift in management behavior.

This is why the framework matters. It is also why it is not, on its own, sufficient.

What This Means for the Valuation Question

The honest position is that the discount reflects a real risk, and that risk has not yet been resolved by the 2023 reform — only addressed at the incentive level.

For the discount to close in any sustained way, three conditions need to become observable in the data over time:

The PB-ROE relationship for central SOEs needs to begin reasserting itself — meaning the R-squared in the high-ROE range needs to migrate from near-zero toward something resembling the broader market figure. This would indicate that the market is starting to credit central SOE returns as belonging to shareholders.

Dividend payout ratios need to continue rising in a way that is incremental and predictable, not episodic. Sustained payout growth would indicate that the cash-flow incentives in the new framework are translating into capital return discipline, not just headline metric improvement.

International institutional capital allocation patterns need to shift. The persistence of the discount is, in part, a function of who is not holding these securities. A measurable change in northbound flows, or in the composition of global emerging-market funds, would indicate that the governance risk repricing is moving from theoretical to actual.

None of these conditions are evident yet. All three are observable, and all three can be tracked.

What Comes Next

This article has identified the source of the discount. The next step is to look at where it is largest — and what the geographic and sector distribution of the discount reveals about the nature of the governance risk being priced.

The discount is not uniform. It concentrates in specific industries — petrochemicals, steel, transportation, construction — at levels that, in some cases, exceed 20%. Understanding why these particular sectors carry the largest discount is the next step toward turning this analysis into something a portfolio manager can act on.

The governance risk is real. The next question is where it is priced most aggressively, and whether that pricing matches the underlying risk — or overshoots it.