Discount #02 — What Changed in 2023: The Reform Framework

In 2023, SASAC introduced a new SOE performance framework linking management evaluation to ROE and cash flow quality. This is what changed — and what it signals for valuation.

Beyond the Valuation Number

The first article established a simple fact: China's central state-owned enterprises have traded near 10x earnings for much of the past decade, against roughly 40x for the S&P 500.

What that article did not address is whether anything has changed to make that discount less permanent.

The answer, based on a structural reform framework introduced in January 2023, is that something meaningful has changed — not in the discount itself, but in the incentive system governing the enterprises that carry it.

The Reform Context: A Decade of Gradual Change

To understand what changed in 2023, it helps to understand what came before.

China's SOE reform has proceeded in distinct phases over the past decade. The early phase, from roughly 2012 to 2018, focused on ownership structure — introducing mixed ownership and reducing state monopoly in certain sectors. A second phase, from 2018 to 2022, emphasized governance mechanisms: board authority, management accountability, and incentive alignment.

Each phase addressed a different layer of the structural discount. But none directly linked enterprise performance to the metrics most relevant to capital markets: return on equity, cash flow quality, and capital efficiency.

That changed in January 2023.

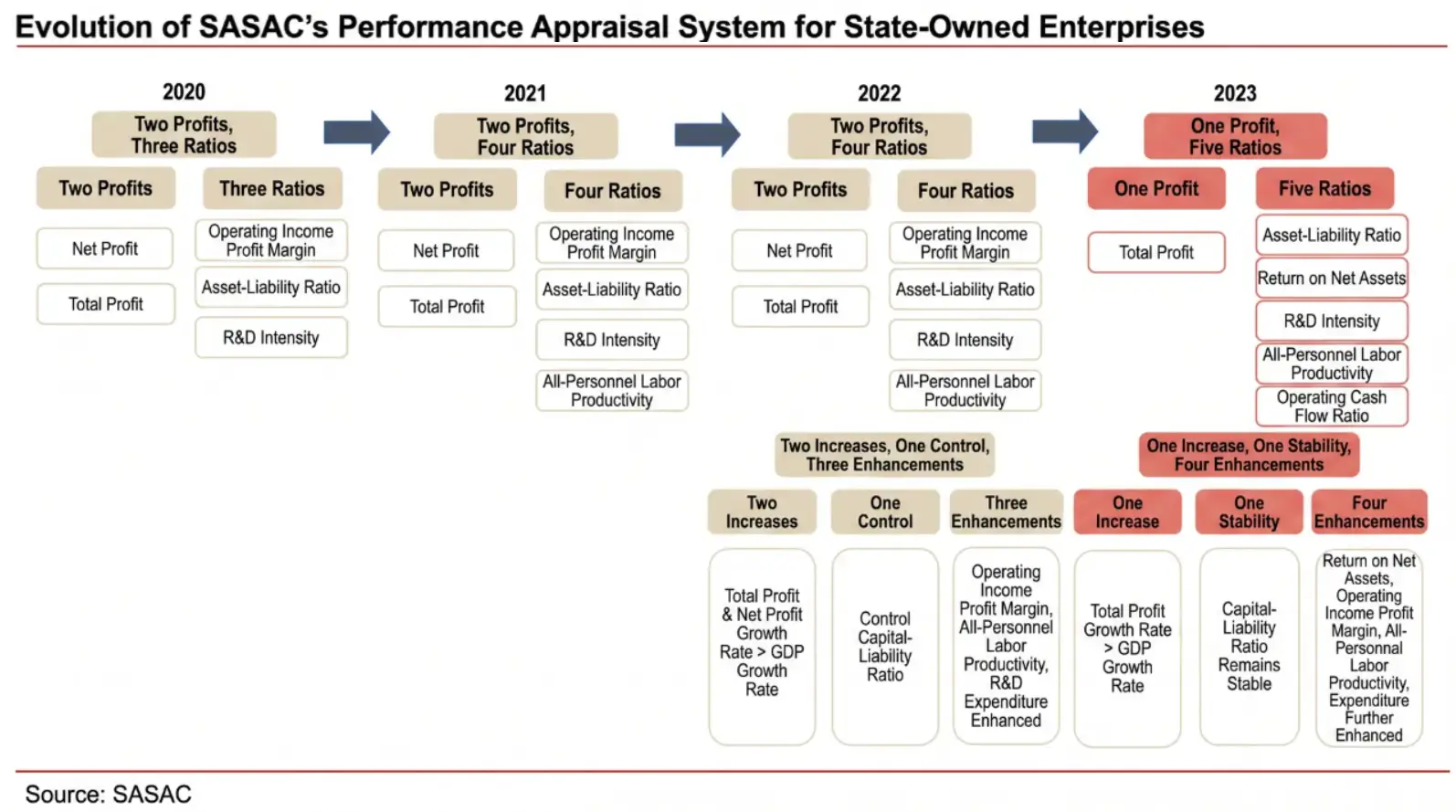

The "One Profit, Five Ratios" Framework

In January 2023, China's State-owned Assets Supervision and Administration Commission (SASAC) replaced its previous performance evaluation system with a new framework known as "Yi Li Wu Lü" — literally "One Profit, Five Ratios."

This is not a marketing slogan. It is a binding performance evaluation system applied to all centrally administered SOEs, directly influencing management accountability and capital allocation decisions.

The framework can be summarized as "One Increase, One Stable, Four Improvements."

The "One Profit": Total Profit Growth

The first element requires that total profit growth exceed the national GDP growth rate.

For global investors, this is familiar territory: it establishes a minimum earnings growth hurdle tied to the broader economy. What matters is that this is now a formal, evaluated target — not an aspiration.

The "Five Ratios": Where the Real Change Lies

The five ratios represent a deliberate shift in how SOE performance is measured. Each deserves explanation.

1. Return on Equity (ROE)

ROE replaces net profit as the primary earnings metric. This is significant.

Net profit measures absolute scale. ROE measures how efficiently capital is deployed to generate that profit. By shifting to ROE, SASAC is explicitly signaling that size is no longer the primary objective — capital efficiency is.

Historically, China's central SOEs have maintained ROE levels above both private enterprises and the broader A-share market average. The new framework is designed to sustain and improve that advantage — with direct management accountability.

2. Operating Cash Flow Ratio

The operating cash flow ratio — defined as net operating cash inflows divided by revenue — replaces the previous metric of operating profit margin.

This change matters more than it might appear.

Profit margins can be managed through accounting choices. Cash flow ratios are harder to manipulate. By requiring SOEs to improve cash flow quality — not just reported earnings — SASAC is pushing enterprises toward more sustainable, verifiable financial performance.

For investors who discount SOE earnings due to concerns about earnings quality, this is a direct response.

3. Asset-Liability Ratio

The asset-liability ratio moves from "controlled" to "stable." This is a subtle but important distinction.

"Controlled" implied a ceiling — a directive to reduce leverage. "Stable" implies managed discipline — allowing SOEs to use debt productively while preventing reckless expansion.

In practical terms, this signals SASAC's support for SOEs to pursue disciplined financing for strategic purposes, without the constraint of a blanket deleveraging mandate.

4. R&D Investment Intensity

R&D intensity — measured as R&D expenditure as a percentage of revenue — reflects a longer-term strategic objective: reducing dependence on foreign technology in critical sectors.

For investors, this metric is less immediately relevant to near-term valuation. But it signals that SOEs are being evaluated not just as cash-generating machines, but as strategic actors in industrial policy.

5. Total Labor Productivity

Labor productivity — measured as output per employee — addresses a long-standing criticism of SOEs: overstaffing and operational inefficiency.

By making this a formal evaluation metric, SASAC is creating direct incentives for SOEs to optimize their workforce structure and improve per-employee output.

Why This Framework Matters for Valuation

The "One Profit, Five Ratios" framework matters because it directly addresses the three factors most responsible for the persistent SOE valuation discount.

First, it shifts the focus from scale to efficiency. ROE and cash flow quality are the metrics global investors use to assess whether capital is being deployed productively. By making these central to management evaluation, SASAC is aligning SOE incentives with the concerns of minority shareholders.

Second, it creates accountability. These are not voluntary targets. They are binding evaluation criteria with direct implications for management compensation and career outcomes.

Third, it improves the credibility of cash returns. Higher and more predictable dividends — supported by improved ROE and cash flow discipline — reduce the uncertainty premium that global investors have historically priced into Chinese SOEs.

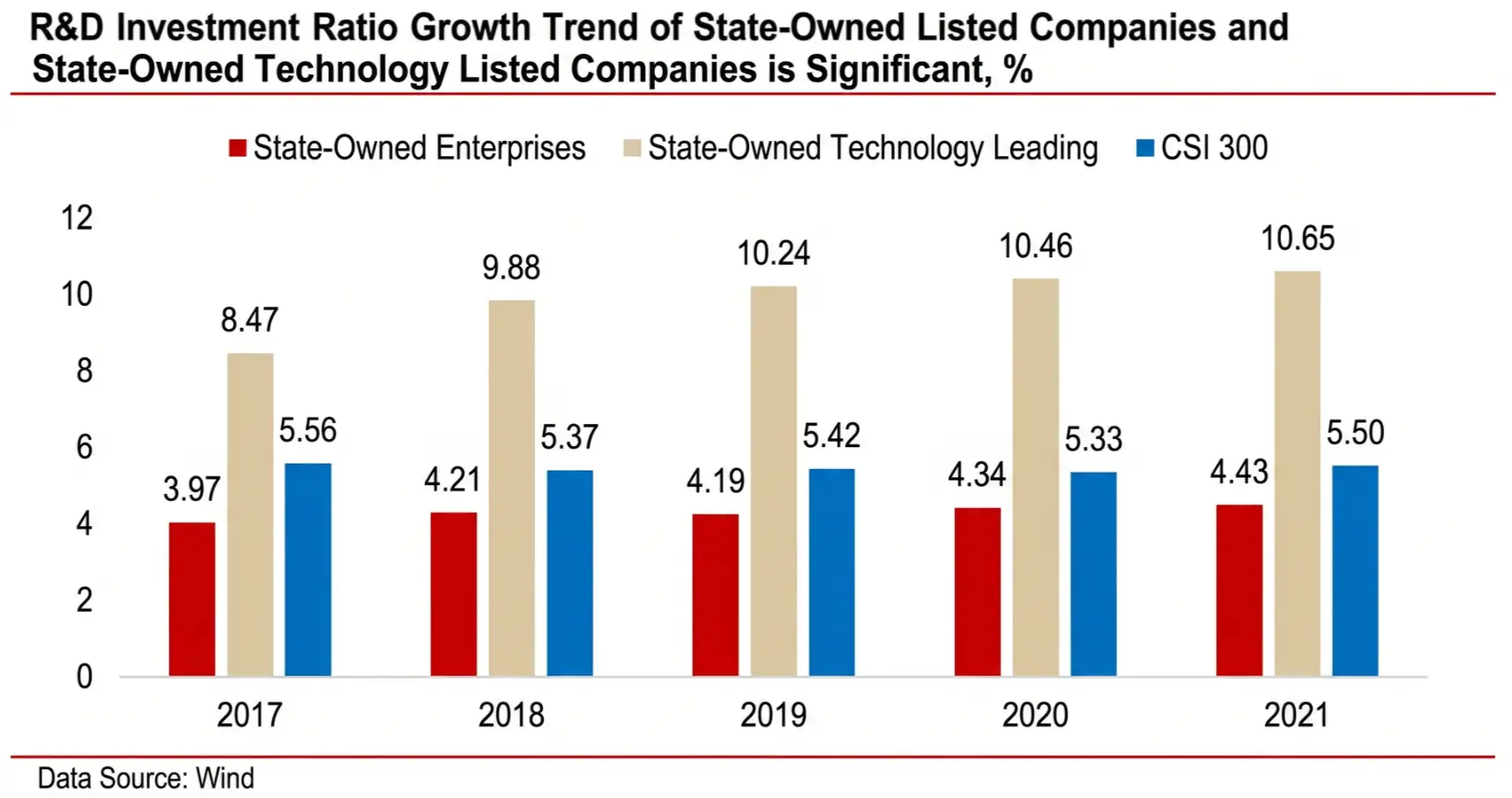

The Data Behind the Framework

The reform framework did not emerge in a vacuum. The underlying data on SOE performance provides important context.

Between 2012 and 2022, central SOEs consistently outperformed broader industrial enterprises on revenue growth, particularly during periods of economic stress. In the first two months of 2023, central SOE revenue grew 5.0% year-on-year, while total profit grew 9.9% — significantly above the comparable figures for China's industrial sector overall.

On ROE, central SOEs have maintained a measurable advantage over both private enterprises and the broader A-share market across most of the past decade — even as the absolute level has declined from its peak.

On dividends, the data is equally clear. As of December 2022, the median cumulative three-year dividend payout ratio for central SOE listed companies was 55.17% — meaningfully above the 49.59% for private enterprises and 46.29% for the broader A-share market.

The valuation discount, in other words, does not reflect inferior fundamentals. It reflects a persistent pricing of control and governance uncertainty.

Why Non-Chinese Investors Should Pay Attention

The "One Profit, Five Ratios" framework is a domestic Chinese policy document. So why should an investor in New York, Toronto, or London care?

The answer lies in what the framework changes about the risk-reward equation.

For years, the SOE discount was justified by a simple argument: these enterprises prioritize stability and policy objectives over shareholder returns, making them uninvestable by conventional capital market standards. That argument had merit.

What the 2023 reform framework does is introduce a formal mechanism that, for the first time, ties management evaluation directly to metrics that capital markets understand: return on equity, cash flow quality, and earnings growth relative to the economy.

This does not guarantee that the discount will close. Governance uncertainty remains real. Policy objectives have not disappeared. And the history of SOE reform suggests that implementation is always the harder part.

But it does change the analytical framework. A market segment that was previously difficult to evaluate using conventional metrics — because the incentives were misaligned with shareholder outcomes — now has a formal, publicly stated performance system that is at least partially legible to global investors.

For investors managing diversified global portfolios, that shift matters. The question is no longer whether Chinese SOEs are investable in principle. The question is whether the implementation of this framework produces the outcomes it promises.

That is a question worth asking — and worth tracking.

What Comes Next

The framework sets the direction. The data will determine whether it is followed.

Future analysis will examine how specific metrics — particularly ROE improvement, dividend payout trends, and cash flow quality — are evolving across central SOE sectors, and what that evolution implies for the structural discount examined in the first article.

Understanding the gap between policy intent and measurable outcome will be essential.