Discount #01 — Why China's State-Owned Enterprises Trade at a Discount

China’s state-owned enterprises trade near 10x earnings, versus about 40x for the S&P 500. A data-driven analysis of the structural valuation gap.

The Discount Nobody Talks About

For years, global investors have debated whether China’s equity market is “cheap.”

What is discussed far less—and often dismissed too quickly—is how large, persistent, and quantifiable that cheapness actually is, especially within China’s state-owned enterprises (SOEs).

As of April 2026, the valuation gap is not subtle. It is structural.

A Valuation Gap That Refuses to Close

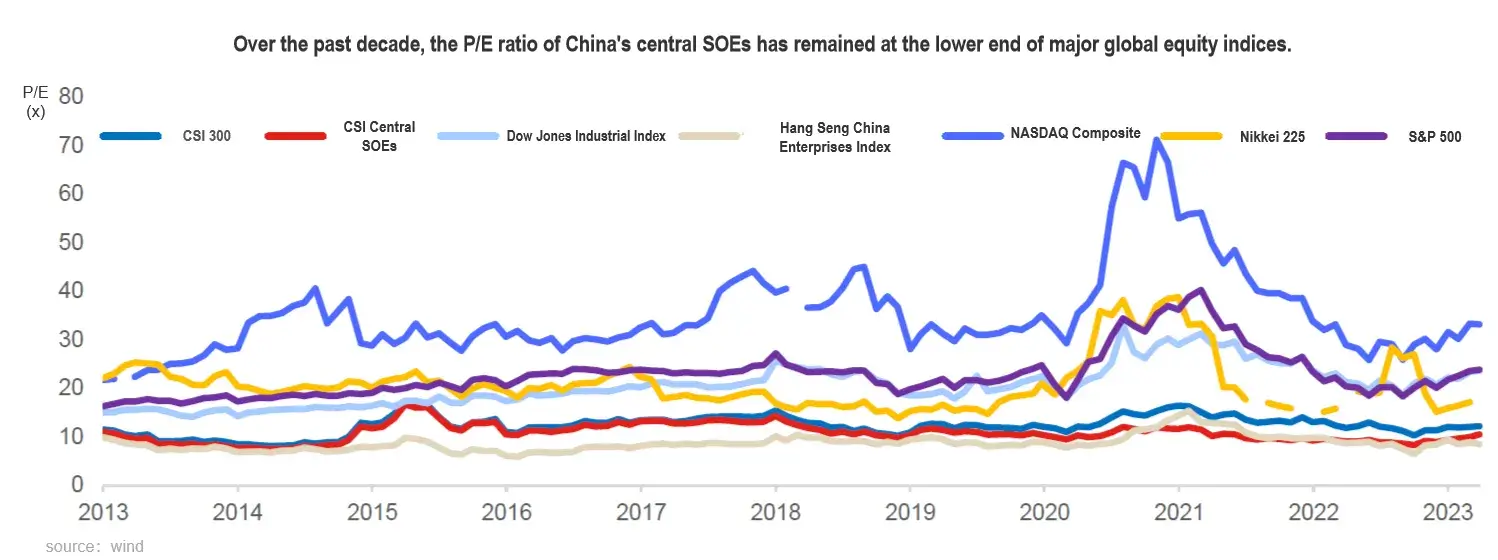

At the index level, the contrast is striking.

China’s centrally administered state-owned enterprises—often tracked through SOE-focused indices—have traded at price-to-earnings ratios around 10x for extended periods.

Over the same timeframe, the S&P 500 has traded close to 40x earnings.

This is not a temporary divergence driven by a single bad year or cyclical earnings volatility. It reflects a long-standing valuation regime.

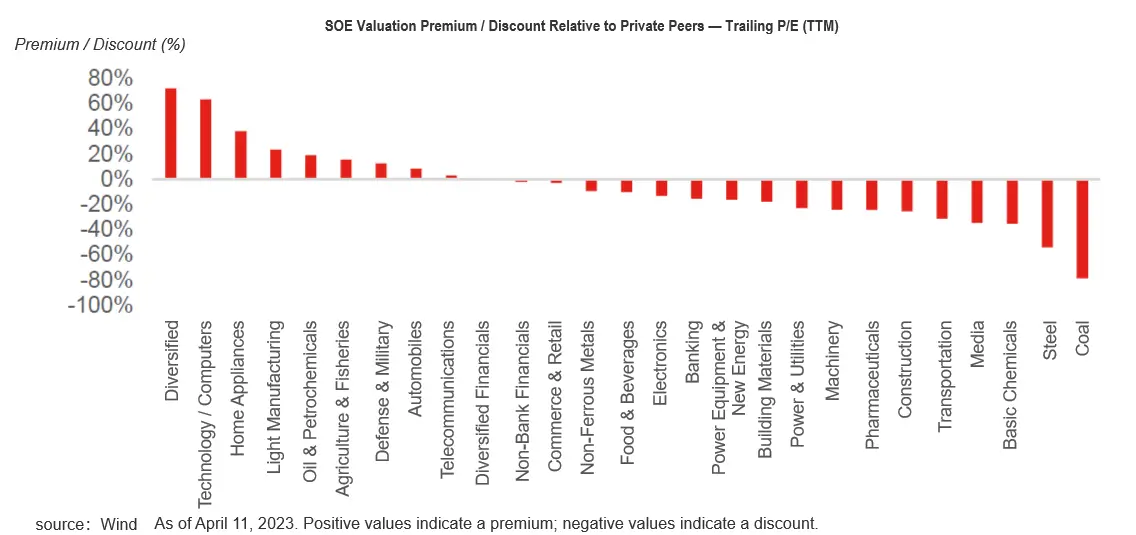

Even when compared domestically, SOEs consistently trade at a discount relative to privately owned peers.

Across sectors such as oil and petrochemicals, building materials, steel, transportation, and logistics, state-owned firms exhibit valuation discounts exceeding 20 percent versus comparable non-state enterprises.

This discount is observable, repeatable, and measurable. It is not an anecdote.

Not a Single-Sector Story

One common assumption is that SOEs are cheap because they are concentrated in “old economy” industries. The data does not support this simplification.

The valuation discount appears across multiple heavy industrial and infrastructure-linked sectors, including : Energy and petrochemicals, Steel and construction materials, Transportation and logistics, Utilities and capital-intensive manufacturing.

In many of these industries, SOEs control strategic assets, dominate market share, and generate stable cash flows. Yet the market assigns them persistently lower valuation multiples than their private-sector counterparts.

The implication is important: this is not just a sector composition effect, but a systematic ownership-based discount.

What the Discount Is—and What It Is Not

It is tempting to attribute this valuation gap to political narratives or short-term sentiment. That approach obscures more than it explains.

The discount is not primarily driven by:

- Temporary earnings weakness

- A single regulatory shock

- Short-term capital flows

Instead, it reflects how global investors price control, incentives, and capital allocation.

SOEs are often perceived as:

- Prioritizing stability over profitability

- Bearing non-commercial responsibilities

- Delivering returns that are less directly aligned with minority shareholders

Whether these perceptions are fully justified is a separate question. What matters, from a market perspective, is that they are priced in—consistently and at scale.

Why the Size of the Discount Matters

A 20 percent valuation discount is meaningful. A valuation multiple that is one-quarter of the S&P 500’s is extraordinary.

At these levels, the discussion should no longer be about whether the discount exists. It should be about whether the market is correctly pricing its permanence.

For North American investors accustomed to debating whether U.S. equities deserve a 22x or 25x multiple, a segment of the world’s second-largest equity market trading near 10x earnings should not be ignored simply because it is uncomfortable or unfamiliar.

A Question Worth Asking

This article does not argue that China’s SOEs are mispriced. It argues that their pricing deserves closer scrutiny.

The discount is real. The scale is large. And the reasons behind it are structural—not cyclical.

Understanding why this discount persists, and under what conditions it could narrow—or fail to—will be critical for anyone attempting to make sense of China’s equity market beyond headlines.

That question will be the focus of the analysis that follows.