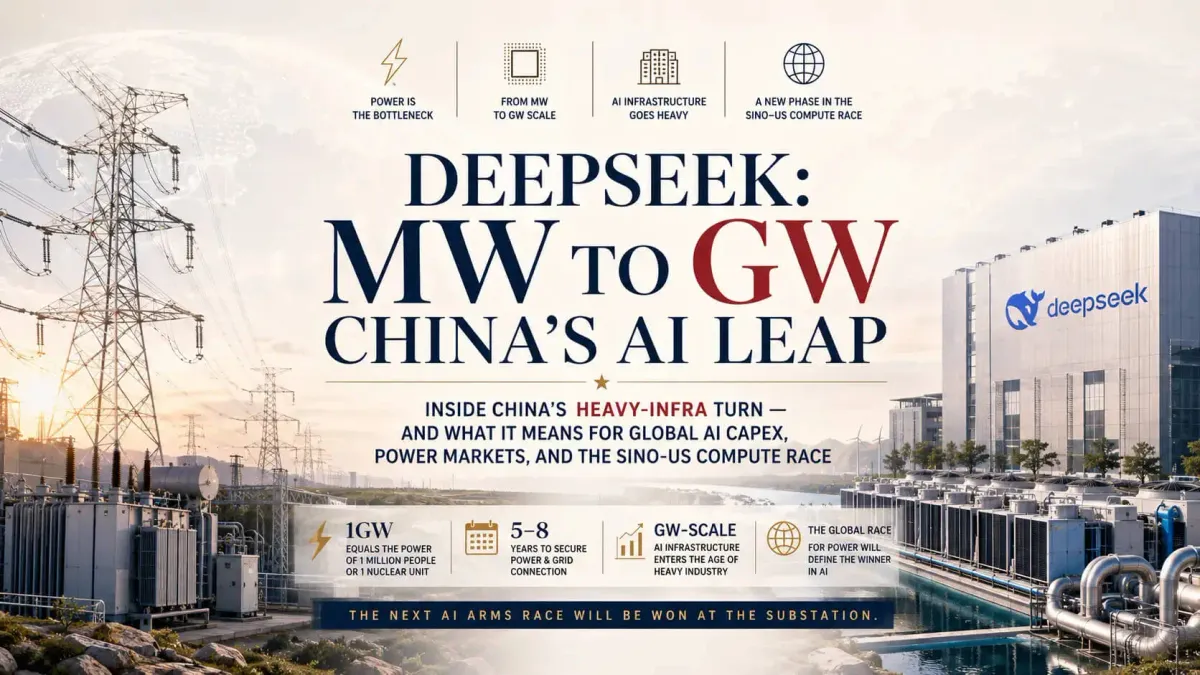

The Stark Signal: DeepSeek Is Building Its Own Gigawatt-Scale AI Infrastructure

DeepSeek targets GW-scale AI infrastructure, marking China's pivot from asset-light research to heavy-asset compute ownership. As AI expansion hits the global power bottleneck, we analyze why this shift puts DeepSeek in the same league as OpenAI’s Stargate and what it means for global investors.

Why a routine job posting reveals China's largest model-maker is entering the heavy-infra phase — and what it means for global AI capex, power markets, and the Sino-US compute race.

DeepSeek, the Hangzhou-based AI lab whose valuation reportedly hit RMB 350 billion (~$48 billion) in its latest funding round, quietly posted a job listing this week for an "IDC Design & Planning Engineer." Most Chinese-language coverage treated it as routine recruitment news.

It is not.

The job description contains a single line that reframes the entire story:

"You will have the opportunity to participate in the planning and construction of infrastructure from MW (megawatts) to GW (gigawatts) scale."

This is the first explicit signal that China's most capital-rich independent AI lab is moving from renting compute to building its own electrical-substation-scale data centers — a transition that puts DeepSeek into the same infrastructure category as OpenAI's Stargate and xAI's Colossus.

For global investors, the implications extend far beyond DeepSeek itself.

Why It Matters

Three structural shifts are embedded in this announcement:

1. The capital structure transition. Chinese AI labs have, until 2025, operated as asset-light research entities renting compute from cloud providers (Alibaba Cloud, Tencent Cloud, government-backed AI computing centers). A move into GW-scale self-built infrastructure means AI is becoming a heavy-industry business in China — closer to utilities and chemicals than to software. This has direct implications for how Chinese AI companies should be valued: not on revenue multiples, but on PP&E plus power supply contracts.

2. The Sino-US compute race finally has Chinese numbers. Until now, Western analysts could only see the US side of the AI infrastructure arms race — OpenAI's Stargate (5GW per campus, 30GW long-term, $100-500B investment), xAI's Colossus, Anthropic's compute deals. China's side has been a black box. A "GW-scale" target in a public DeepSeek job posting is the first explicit anchor. If DeepSeek alone targets GW-scale, then Alibaba's AI infrastructure (much larger), ByteDance's Doubao infrastructure (larger still), and state-backed China Computing Network are likely a multiple of that.

3. Global power infrastructure is the real bottleneck. The job posting buries a quiet observation: in current AI infrastructure economics, building the data center takes 1-2 years; getting grid connection and power supply takes 5-8 years. This is true in China, in the US, and in Europe. The investable thesis is not "who builds the most data centers" but "who controls the power."

The International Comparison

To calibrate how aggressive DeepSeek's GW-scale ambition is, look at the publicly disclosed numbers from US peers:

|

Project |

Operator |

Power Capacity |

GPUs |

Investment |

|

Stargate |

OpenAI × Microsoft × SoftBank |

5GW/campus, 30GW total |

Millions |

$100-500B |

|

Colossus 1 |

xAI (Memphis, TN) |

~300MW |

230,000 |

undisclosed |

|

Colossus 2 |

xAI (Memphis, TN) |

claimed 1GW, est. ~350MW |

scaling |

undisclosed |

|

Hyperion |

Meta (Louisiana) |

2GW+ planned |

undisclosed |

$10B+ |

|

DeepSeek |

DeepSeek (multi-site) |

"MW to GW" range |

undisclosed |

undisclosed |

For context: a single 1GW data center consumes the electricity equivalent of a city of one million people, or one full nuclear reactor unit. Prior to 2023, "hyperscale" data centers globally averaged 50-100MW.

The leap from MW-scale to GW-scale is not incremental — it is a category change. It puts AI compute on par with primary aluminum smelting or hydrogen electrolysis in terms of grid load.

The Bottleneck Few Investors Are Pricing In

The headline-grabbing storyline in 2024-2025 was the GPU shortage. By 2026-2027, the binding constraint will be electrical power, not silicon.

Three reasons:

Grid interconnection queues are years long. In the US, PJM Interconnection (the grid operator covering 13 states) currently has a 5-7 year backlog for new large-load connections. In China, the situation varies by province — Inner Mongolia and Ningxia (where DeepSeek already has a presence in Wulanchabu) have ample renewable capacity but require transmission infrastructure to monetize it.

Transformer and switchgear supply is constrained globally. Large power transformers have 18-24 month lead times. Some specialty equipment (HVDC converter stations, ultra-high-voltage transformers) has 36+ month lead times. This is the global supply chain that AI compute is now competing with industrial customers for.

Cooling water and grid capacity are local constraints, not global. Even where the grid has capacity, sourcing 1GW of dispatchable power adjacent to a fiber-rich, cooling-water-rich location is non-trivial. This is why hyperscalers are increasingly co-locating with nuclear plants (Microsoft × Three Mile Island, AWS × Talen Energy) or natural gas peakers.

DeepSeek's job posting acknowledges this implicitly — it lists "liquid cooling, high-density power distribution, modular construction, and intelligent operations" as key research areas. These are not nice-to-haves; they are the only path to deploying GW-scale compute within reasonable timeframes.

Investment Implications

This signal has three layers of investable consequences:

Layer 1 — China A-share opportunities.

Chinese suppliers in the AI infrastructure value chain are likely to see capacity-driven multi-year demand:

- Liquid cooling: Envicool (002837.SZ), Yinlun Machinery (002126.SZ)

- Power transformers and switchgear: XJ Electric (000400.SZ), TBEA (600089.SH)

- HVDC transmission: NR Electric (300831.SZ), Pinggao Electric (600312.SH)

- Modular data center construction: Aofei Data (300738.SZ), Sugon (603019.SH)

- Nuclear / power generation: China National Nuclear Power (601985.SH), Yangtze Power (600900.SH)

These names share a common attribute: they have been trading at structural valuation discounts (the very thesis Ashare Insights has been documenting in the Discount series). A multi-year AI-driven capex cycle changes the demand picture without requiring SOE reform to play out.

Layer 2 — Global power and infrastructure plays.

The bottleneck is global, and the investment logic externalizes:

- US utilities with AI data center load: Vistra (VST), Constellation Energy (CEG), Talen Energy (TLN)

- Uranium: Cameco (CCJ), Sprott Physical Uranium Trust (U.UN)

- Grid equipment: GE Vernova (GEV), Hitachi Energy

- Specialty natural gas: Williams Companies (WMB), Energy Transfer (ET)

Layer 3 — The compute-cost differential.

If Chinese AI labs can build GW-scale infrastructure at meaningfully lower marginal cost than US peers (cheaper land, cheaper power, cheaper labor, vertically integrated supply chain), the long-term cost-per-inference advantage compounds. This is the underappreciated structural story behind DeepSeek's models being significantly cheaper than US peers on a per-token basis. It is not just algorithmic efficiency — it is infrastructure cost arbitrage.

What to Watch

Three signals to monitor over the next 6-12 months:

- Whether DeepSeek publicly discloses specific GW figures. Chinese AI labs have historically been opaque about infrastructure capex. A move toward US-style infrastructure disclosure would be a major signaling event.

- Provincial-level power allocation announcements. Inner Mongolia, Ningxia, Guizhou, and Sichuan are the four provinces most likely to host GW-scale AI infrastructure. Watch for NDRC (National Development and Reform Commission) bulletins on AI data center power quota allocation.

- The next round of Chinese hyperscaler infrastructure disclosures. Alibaba (BABA) Q3 capex, Tencent (0700.HK) Q3 capex, and ByteDance's Doubao infrastructure spending will reveal whether DeepSeek's move is an outlier or the leading edge of an industry-wide pivot.

DeepSeek's job posting will not move markets this week. But six months from now, when Chinese AI labs collectively disclose double-digit billion-dollar infrastructure budgets, this announcement will be remembered as the first public indicator that the second phase of the AI capex cycle — the heavy-infrastructure phase — has begun in China.

The first phase enriched Nvidia. The second phase will enrich whoever builds the substations.