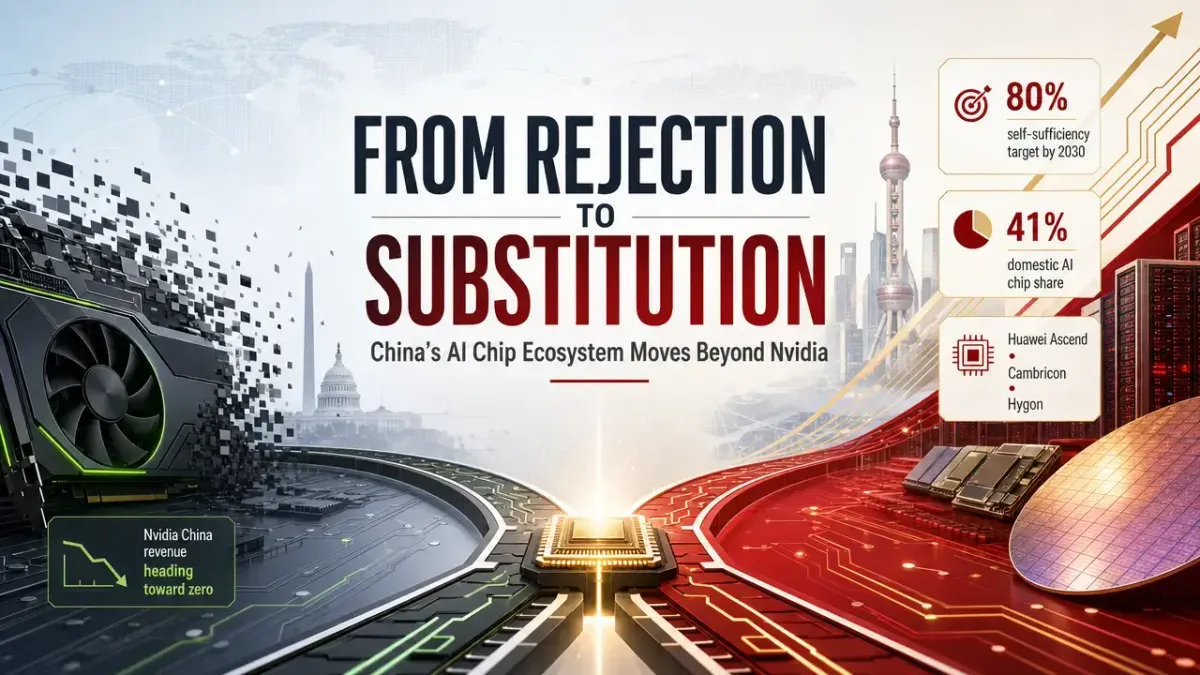

China Stops Buying Nvidia's Approved Chips — and That's the Bigger Story

Beijing didn't just block another product. It refused to place orders for chips Washington had already approved. That shift from rejection to substitution is what matters.

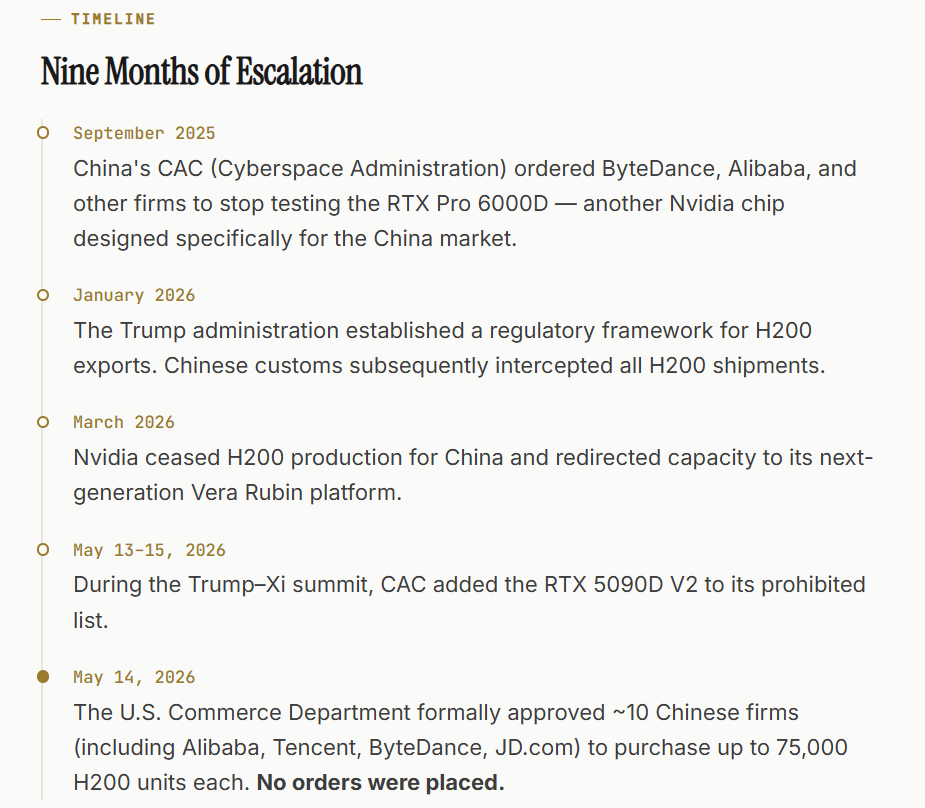

Jensen Huang joined President Trump's delegation to Beijing hoping to break the deadlock on chip exports to China. He left with a different kind of signal: Beijing listed Nvidia's China-specific RTX 5090D V2 gaming GPU on its own ban list — during the summit.

That was not an isolated event. It was the latest in a nine-month escalation where both governments tightened restrictions, but where Beijing's posture shifted from defensive to strategic. The evidence: when Washington approved up to 75,000 H200 units each for roughly 10 Chinese companies, none of them placed an order.

Timeline

Nine Months of Escalation

President Trump acknowledged the situation on his return flight: "They chose not to buy because they want to develop their own." U.S. Trade Representative Greer confirmed that chip export controls were not even a primary agenda item in the bilateral meetings.

Analysis

From Rejection to Substitution

Beijing's strategy has moved past simply blocking U.S. chips. The current posture is to actively build alternatives — and the targets are now written into national planning.

Key commitmentChina's 13 top semiconductor companies have pledged to reach 80% chip self-sufficiency by 2030, up from an estimated 33% in 2024. This target is codified in the 15th Five-Year Plan (十五五规划).

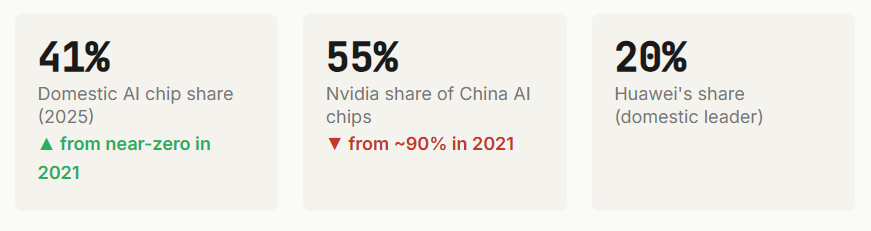

In AI chips specifically, the shift is already measurable. Domestic players captured 41% of China's AI chip market last year, compressing Nvidia's share to 55% — down from near-monopoly just three years earlier.

Among domestic players, two stand out:

- Huawei leads with ~20% market share via its Ascend series, deployed heavily across state-owned telecom and cloud infrastructure.

- Cambricon (寒武纪) reported its first profitable quarter in 2025. Goldman Sachs projects its AI chip shipments will scale from 143,000 units to 2.1 million by 2030 — a 14x increase. (Source: Goldman Sachs China Semiconductor Outlook, March 2026)

Data

By the Numbers

| Metric | 2024 | 2030E |

|---|---|---|

| Overall chip self-sufficiency | 33% | 80% |

| Domestic AI chip share (China) | 41% | 76%* |

| Nvidia share of China AI chip market | 55% | — |

| Nvidia China revenue share | ~13% | ~5% |

| Cambricon AI chip shipments | 143K | 2.1M |

| * Morgan Stanley estimate. All other 2030 figures from company pledges / 15th FYP targets. Nvidia revenue share from company filings. | ||

What changed at NvidiaNvidia's latest quarterly guidance assumes zero revenue from China for the current quarter. China accounted for approximately 13% of total revenue two years ago; that figure has fallen to roughly 5% and is headed toward zero in the company's forward planning.

Implications

What It Means

1. For Nvidia: The "compliant chip" playbook is exhausted

Huang's three-part strategy — design chips that comply with U.S. rules, get Washington to approve them, get Beijing to allow them in — has reached its limit. Beijing is no longer passively accepting approved products. It is actively rejecting them to accelerate domestic alternatives. Nvidia's assumption of zero China revenue is not conservative; it is the base case.

2. For Chinese semiconductor names: From concept to earnings validation

Cambricon's first profitable quarter is a meaningful milestone. Companies like Huawei (private), Cambricon (688256.SH), and Hygon (688041.SH) are transitioning from policy-driven narratives to revenue-driven ones. The 76% domestic share projection from Morgan Stanley is aggressive, but the direction of travel is clear. Watch for: government procurement mandates, state-owned cloud deployment commitments, and sequential revenue growth in quarterly filings.

3. For global AI infrastructure: A dual-track supply chain is forming

The U.S. and China are building parallel AI computing ecosystems with decreasing interdependency. For global investors, this means: (a) China-related revenue assumptions for Western semiconductor companies need to be stress-tested near zero; (b) Chinese cloud and AI companies will increasingly deploy domestic silicon, creating a data-center buildout cycle that benefits local equipment suppliers; (c) third-market countries may face pressure to choose between U.S. and Chinese AI infrastructure stacks.

Risks to monitorSelf-sufficiency targets are aspirational, not guaranteed. China's 80% target by 2030 assumes sustained government funding, talent availability, and no major technology bottlenecks in advanced lithography. A single bottleneck — e.g., EUV equipment access — could slow progress significantly. Additionally, domestic chips still lag Nvidia on performance per watt for large-scale training workloads. The substitution thesis works for inference and fine-tuning; it is less proven for frontier model training.

Disclosure: The author holds no positions in any of the securities mentioned. This is not investment advice.

Sources: CAC announcements, U.S. Commerce Department filings, Nvidia quarterly earnings (Q1 FY2027), Morgan Stanley China Semiconductor Outlook (March 2026), Goldman Sachs China Semiconductor Research (March 2026), 15th Five-Year Plan (十四五/十五五规划) text.